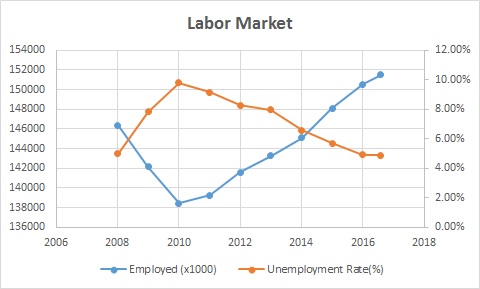

Well recognized think tank Brookings released a report recently, which looks very wrong to me. Brooking claims that lower unemployment by 1% raises traffic deaths by 14%. (See Fig 1 and Fig 2) Brookings reasoned when employment rate goes down, newly hired workers tend to cause more traffic death, therefore the relationship of unemployment rate and traffic death toll.

Fig. 3 shows that traffic death did go up significantly in 2015. Evidently, unemployment rate in 2015 is similar to 2005, around 5.2%. But it's clear that traffic death in 2015 is way less than 2005, which is apparently inconsistent with Brookings' theory. At least Brookings' theory doesn't apply for long term period of time.

Fig. 4 shows that traffic death in 2016 is up a lot too. Unemployment rate is down by about 0.5% relatively to the first six months in 2016. This seems to match Brookings' theory roughly. But there are other crucial factors related to traffic death.

First, crude price started to fall in the end of 2014 rapidly to below $50/Barrel from around $100/Barrel, and even close to $30/Barrel at one point. Fig. 5 shows vehicle mileage goes up when crude oil price goes down. This is easy to understand because consumers can drive more while still save some money from gasoline as the price of oil has gone down so much. Increase of traffic death in 2015 and 2016 is apparently related to the drop of oil price and the increase in use of vehicles.

Secondly, 2015 and 2016 are the years of record high number of car sales since 2008 financial crisis. With more vehicles on road and more crowd road condition, undoubtedly traffic accidents happen more often, and hence the increase of traffic death.

On the flip side, it's certainly impossible to rule out entirely that newly hired workers in economic recovery cycle are worse drivers than normal. But there is still a math problem for Brookings' theory. If 1% of newly employed workforce are all terrible drivers, and they cause 14% increase in traffic death overall, as Brookings claims, the bad drivers have to have 14 times worse than normal drivers, mathematically. 14 times worse, 14 times killing rate! How could that be possible?

To conclude, Brookings' highly advertised research product is really a joke. It's hard to have confidence in academic authorities these days.

Figure 1 Brookings' conclusion

Figure 2 Brookings' promotion on Twitter

Figure 3 Traffic death over the years

Figure 4 Traffic death of first six months

Figure 5 Vehicle mileage change(YOY)/right axis

and crude price/left axis

(go homepage to read more)

(All rights reserved)